Home / Insurance Claims / The Process

— Insurance Claims Process · WI & IA

The claim process, demystified.

A roof or storm insurance claim sounds intimidating, but it's a predictable set of steps. Here's exactly how it works, who does what, and where we take the weight off you. You pay your deductible, we handle the rest.

Free claim help

WI & IA · We respond in 2 hours

Start the claim the right way.

Most claims succeed or fail on the first two steps, inspection and documentation. Start there, free, and we'll set the claim up properly and carry it through with your carrier. We respond within 2 hours, 24/7 for emergencies.

— The Process, Step By Step

SEC 01 / 07

Six stages, and who does each one.

The whole point is that you're not doing this alone. Here's every stage of a roof or storm claim, with exactly what's on us and what's on you.

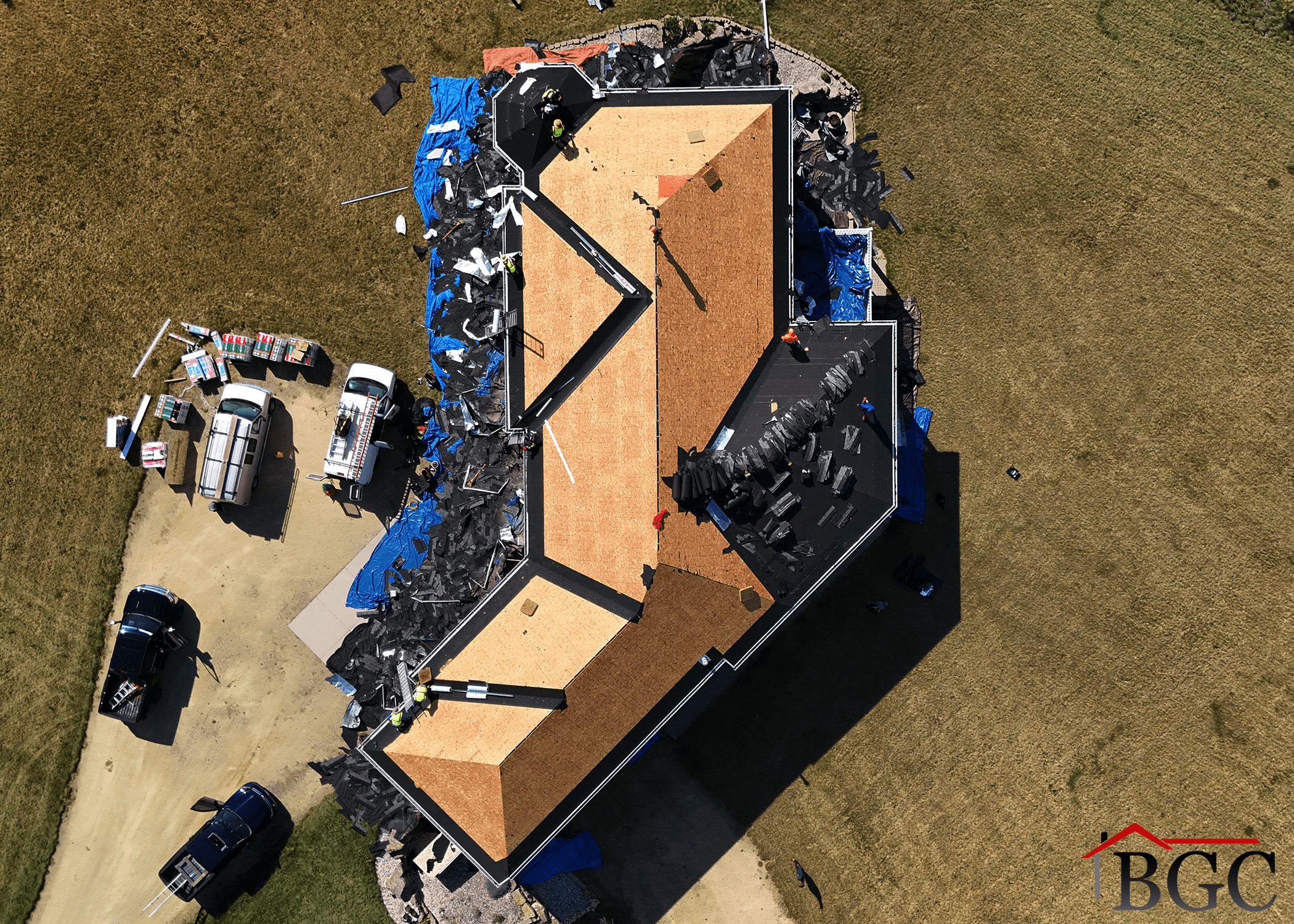

Free damage inspection

It starts with knowing what you're actually dealing with. We inspect the roof, siding, and gutters and tell you honestly whether there's damage worth a claim, no pressure

Documentation

This is where claims are won. We photograph and document the full scope of the damage in the format your adjuster expects, so nothing legitimate gets left out. We handleP

File the claim

You contact your insurer to open the claim, it's your policy, so this step is yours, but we tell you exactly what to say and provide so it starts clean. We handleGuide yo

The adjuster visit

Your insurer sends an adjuster to assess the damage. We meet them on-site and walk the damage together, so what they scope matches what's actually there. We handleMeet th

Approval & scope

The carrier issues its decision and a scope of covered work. We review it against our inspection to confirm it reflects the real damage, and flag anything missing. We han

Repair & completion

Once it's approved, our own crews complete the work to the agreed scope, and we handle the final paperwork so the job closes cleanly. We handleThe full repair with our ow

— Claim Terms, In Plain English

SEC 02 / 07

The words on your claim, decoded.

— You Vs. Us

SEC 03 / 07

— What To Expect

SEC 04 / 07

How long does a claim take?

Every claim is different, and timelines depend on your carrier and the damage. But here's the honest shape of it, and where we keep things moving.

Inspection & documentation: usually days

We respond to inspection requests within 2 hours and can typically inspect and document quickly, often within a few days, sooner if it's an emergency that needs tarping f

Adjuster & approval: carrier-dependent

This stage is in your insurer's hands, scheduling the adjuster and issuing a decision can take anywhere from days to a few weeks. We keep it moving by meeting the adjuste

Repair: scheduled once approved

After approval, we schedule the repair with our own crews and complete it to the agreed scope, then handle the closing paperwork, including any recoverable depreciation.

— What Homeowners Say

Reviews

Posted on GoogleTrustindex verifies that the original source of the review is Google. When the big storms came through the Madison-area in April 2026, I immediately started looking for a reputable roofer—who also understood the importance of weather-resistant materials that can withstand hail and wind. It didn’t take me long to find Brad from BCG. We had damage that needed to be repaired before the next round of storms came through later that day and Brad had a crew out within hours. Our neighbors also had damage, and when their roofing company didn’t show up, Brad and his crew also took on fixing their damage on the spot. The contracting process was done over email and we were able to clearly understand all of the options available to us. On the day of install, the crew was efficient and fast with their work. But also, mistakes can happen. And what matters to us is not that there’s perfection (because that’s not realistic), but how a contractor deals with a mistake. As they were taking down the tarps when they were finished with the roof, one of our lights next to the garage broke. Brad helped find a replacement online and had it shipped directly to our house! Such great service! All in all, we were very happy with Brad and the service we received from him and BCG. We’ve since recommended their services to several of our friends and neighbors who also had storm damage. While I hope we won’t have to do that again for a long time, we would work with BCG again in a heartbeat!Posted on GoogleTrustindex verifies that the original source of the review is Google. I am extremely pleased with the service Matt Walmer from Buckshot General Contracting (BGC) provided for me during the hailstorm damage in Madison in April. I had just switched insurance companies one year ago and was worried about how much they would cover. Matt assured me everything would be taken care of and had nothing to worry about. True to his word he immediately answered phone calls during off hours even when he was with daughter at volleyball and answering texts in seconds Matt met up with assessor and arrived 20 minutes early. During roof replacement he stopped in 3 times to check the progress and next day he came back to do a walk around to make sure the cleanup was to his standards. I have been so blessed to work with Matt at BGC as my contractor as everything went so smoothly. No problems with my insurance company and I was the first one on my block to get my roof done. I also was telling Matt about some of my neighbors having problems with their insurance and he was willing to look at their paperwork and giving them advice on how to deal with them. I can proudly say I announced to them how good Matt was and gave them his card. Thank you so much Matt for your excellent service and being a great representative for Buckshot General Contracting. These days days it’s hard to find a business that is 100% committed to making sure the customer is their #1 concern. Going to be doing more work and sticking with them as I know it will be top quality.Posted on GoogleTrustindex verifies that the original source of the review is Google. We contacted BGC after storm damage and had them completely re-roof and re-side our house, garage, and shed. The entire process was incredibly smooth from start to finish. They were easy to work with, handled all the details, and made what could have been a stressful situation completely worry-free. Our contact, Jayce Kirkland, was outstanding. His professionalism, communication, and courteous demeanor were truly a breath of fresh air. He took care of everything for us and made sure the project stayed on track every step of the way. We couldn’t be happier with the experience and have and would highly recommend BGC to anyone needing roofing or siding work!Posted on GoogleTrustindex verifies that the original source of the review is Google. Very customer focused company. Replaced my roof and siding after hail and wind damage 6 years ago. Second hail and damage storm this year and they are my vendor of choice again. In process now to replace my roof and siding.Posted on GoogleTrustindex verifies that the original source of the review is Google. Brad gave me a good price and the roof looks great! The roof was replaced in one day.Posted on GoogleTrustindex verifies that the original source of the review is Google. They did an excellent job! Fast, efficient and did a great job cleaning up.Posted on GoogleTrustindex verifies that the original source of the review is Google. My family member needed a roof replacement after the recent storm in Madison , Chad came out to inspect the roof and went over the options with us. Full roof replacement and the new roof looks GREAT, they were done with in 2 days and left no mess behind which was very thankful for. Thanks !!Posted on GoogleTrustindex verifies that the original source of the review is Google. *update* number 2 I have been through about 4 different people now to get my issue fixed. They came and fixed the side that was leaking. The contractor that came out confirmed the siding wasnt installed properly and put in some flashing to fix the issue. Since it wasnt installed right i wanted the rest of the house done to prevent other issues and the company agreed to do that. Still not done and now im dealing with yet another person who has not contacted me to resolve my issue. Told them when this job was completed i wanted a new patio door as well to get the last year of the energy credit. Crickets. I have been very patient, but am beyond frustrated at this point. *update* After posting i was contacted regarding my review. Turns out the reason i wasn’t contacted was because my salesman is no longer with the company and never responded to tell me that when i called him (his number was still correct at the time of the call). I had a rep come to my home and immediately discuss solutions to the issue. Everything was done properly on my home, its just one of those things no one could foresee. I am beyond happy with the speed things are moving once i was contacted. Already making plans for additional work needed next season. Had windows and siding done. The windows crew was fantastic. Personable as well as professional. Siding crew was also great. My issue comes with the after care. My basement was leaking during rains. It also leaked running the sprinkler for new grass. Contacted my salesman and never heard back. Been probably a month? Had a contractor friend of mine come look and the issue was the siding wasnt ran low enough (or a piece of flashing would have worked as well) to stop water from coming through the basement from under the sill plate. Id have even paid to have it corrected, but no call. My issue is a simple one, but the aftercare deserves a one. The total score is because their crews were great. The people in admin simply need to be better. I had to remove foam that was trafficking water in and will be using flex seal to create a barrier since no call was made back. Update as of april, 2026. After some frustrating back and forth one of their contractors came our and looked at my situation late summer of 2025. Confirmed the siding wasnt done properly and installed flashing where the leak was and i haven’t had an issue since. Despite the numerous tornados weve had. With that said, Fall of 2025 i told them (after being informed the siding wasn’t done properly by their guy) i told them while the basement no longer seems to leak, i want the rest of the house covered with that flashing incase their are other problems. i dont want to refinish my basement to discover issues. The “salesman” essentially accused me of only wanting free things and after him explaining to me how awesome he was and that i was wrong, i stopped the phone call. The subcontractors they hire are overall solid, but some of the staff have made the company unusable for me. Just be cautious if you use them. Communication is great… until they get your money.

— Home Base

Madison, WI · Centerville, IA

— Insurance Claim FAQ

SEC 06 / 07

On a covered claim, your deductible is typically your only out-of-pocket cost, you pay your deductible, and we handle the rest with the carrier. Your exact deductible is set by your policy. Coverage is always determined by your insurer.

Usually, yes. A free inspection tells you whether there’s damage worth a claim and gets it documented properly first, so you’re not filing blind or opening a claim that gets denied. We give you an honest read either way. See stage 1 →

Yes, we work with any insurance carrier. We’ve handled claims across major carriers and programs for 47 years, and we meet your adjuster on-site so the scope reflects the real damage.

The adjuster is sent by your insurer to assess the damage and determine what’s covered and the scope of work. We meet them on-site and present our documentation so legitimate damage isn’t missed or underscoped. See stage 4 →

It happens, sometimes damage is missed or underscoped. We can re-inspect, document thoroughly, and provide our findings to support a reinspection or supplement with your carrier. Note we are a contractor, not a public adjuster (see below).

No. We are a licensed contractor, not a public adjuster, and in Iowa we do not offer public adjusting services (Iowa Code §522C). We document damage, complete the repairs, and work alongside your carrier and adjuster as your contractor.

— Related

SEC 07 / 07

Storm & insurance resources.

Free Inspection · Any Carrier

Let's start the claim the right way.

Request a free inspection and we'll confirm the damage, document it for your claim, meet your adjuster, and complete the repair with our own crews. You pay your deductible, we handle the rest. Family-owned since 1979, any insurance carrier.

This page explains the general insurance claim process for educational purposes and is not legal, financial, or insurance advice. Insurance coverage, claim approval, scope, depreciation, and out-of-pocket cost depend on your policy, deductible, and the documented cause and extent of damage; coverage is determined by your insurer, not by Buckshot, and outcomes vary by claim. Buckshot is a licensed contractor and is not a public adjuster; we do not adjust claims or negotiate settlements on your behalf, and we are not Iowa public adjusters nor do we offer public adjusting services (Iowa Code §522C). We document damage and complete repairs, working alongside your insurer and adjuster. WI Lic. DC-080900045 · IL Lic. 104017198 · Family-Owned Since 1979.